Commercial reality has kicked in, with the Australian market reflecting the global trends.

Global digital health investment is contracting, highlighting a rapid structural shift toward consolidation, tighter evidence requirements, and growing control by health systems, according to a new market analysis.

The latest quarterly report from Galen Growth showed venture funding for digital health fell modestly in the first quarter of 2026, but deal volumes dropped sharply as investors concentrated capital into a smaller number of companies.

Emma Hossack, CEO of the Medical Software Industry Association, told HSD the report reflected what she was seeing across the Australian digital health market.

“Commercial reality has kicked in,” she said.

“The update does seem to reflect a more responsible and realistic marketplace where the value is not always the sparkly new idea, but the tech which has runs on the board, a genuine footprint, and evidence of sustainability.

“The stars should always have been the health systems.

“The purpose of health tech is to serve them through better safety and efficiencies, not exhaust them with ideas which sometimes do not reflect or address key funding requirements or business case for clinical change, which has to be overwhelming given the justifiable friction for change in the sector.

“Our industry has been going in this direction for some time now.”

Total venture funding globally reached $7.1 billion across 216 deals, down 6.6% year-on-year, while deal count nearly halved, according to the Galen report. At the same time, the average deal size surged 87% to $38.4 million, reflecting a shift toward larger, higher-conviction investments.

The result was a market no longer driven by rapid expansion and speculative growth, but by what the report described as “focused, high-conviction, operationally disciplined” companies.

“The money is flowing into a rapidly shrinking number of high-conviction transactions,” the report noted, pointing to a clear divide between a small cohort of well-funded players and a long tail of companies struggling to attract capital.

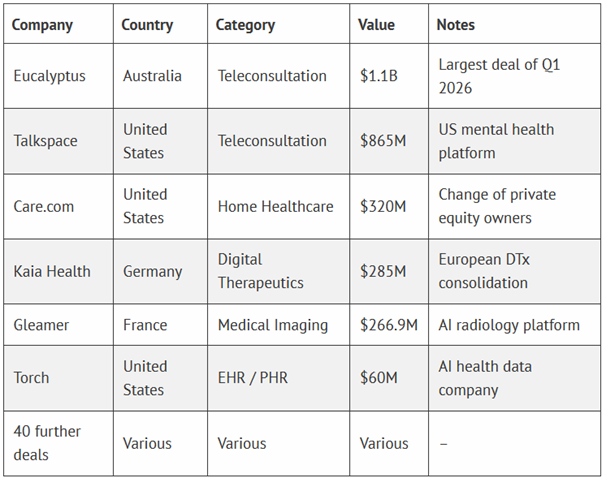

At the same time, consolidation accelerated across the sector, with 46 mergers and acquisitions recorded in a single quarter, making M&A the dominant exit path for digital health companies.

The biggest M&A globally was an Australian one – telehealth provider Eucalyptus’ $1.6 billion acquisition by Californian behemoth Hims and Hers, announced in February.

Source: Q1 2026 M&A Transactions (selected). Source: HealthTech Alpha Premium.

This reflected a broader shift in how value is being realised, with acquisitions and strategic transactions increasingly replacing IPOs as the primary route for investors to exit.

Importantly, much of this consolidation was being driven not by venture capital, but by health systems, payers and large corporates absorbing smaller digital health providers.

The Galen report suggested this marked a fundamental change in the structure of the market, with fragmented digital solutions being rolled up into integrated platforms that aligned more closely with clinical workflows and system needs.

That shift was part of a broader realignment in the balance of power across the sector, it said.

“The most consequential structural shift … is the inversion of the buyer-seller dynamic,” the report stated, arguing that health systems were now acting as “kingmakers” in the market.

Bronwyn Le Grice, CEO of health tech accelerator ANDHealth, said health systems had always been “the kingmakers” in the Australian sector.

“While there is still a fair amount of hype in the broader digital health space, especially as AI takes hold, there is a growing core of highly disciplined, evidence-based companies in Australia,” she told HSD.

“These founders are singularly focused on developing the clinical and commercial evidence to change how we deliver health and care.

“The shift towards fewer, larger, later stage deals is also happening here in Australia.

“Some of this is likely in response to the major correction in digital health valuations which occurred after the pandemic, leaving many investors wary of the sector, but it also reflects the broader tightening of risk capital in the face of global volatility and uncertainty.

“Australia’s regulatory framework has always required significant clinical evidence in order to substantiate claims made by health technology companies, including digital health,” said Ms Le Grice.

“From a company perspective, clinical evidence and regulatory clearances offer a pathway to a stronger competitive moat. However, health economic evidence and commercial validation demonstrating near-term ROI (e.g., within 12 months for the US market) is often overlooked and is essential to navigating complex procurement and reimbursement pathways.

“Health systems have always been the kingmakers in digital health but in many cases the startup community is only just now catching up to that reality.

“Technology-driven companies are often singularly focused on end users, but in health your end user and paying customer are often not the same.

“The companies succeeding now are those that recognise they need to solve both economic and clinical problems simultaneously, without adding friction to an already overburdened system.”

Where venture capital once dictated the direction of innovation, digital health companies were now being shaped by the operational requirements of healthcare providers, including procurement processes, interoperability standards and demonstrable returns on investment, said the Galen report.

This had significant implications for the types of companies that were succeeding.

Related

Rather than broad, platform-based offerings, investors were increasingly backing solutions that addressed specific clinical workflows, reduced administrative burden, and delivered measurable outcomes.

The tightening of evidence requirements was also playing a critical role in this shift.

According to the report, regulators and payers across major markets were raising the bar for digital health reimbursement, with growing expectations for randomised controlled trials or robust real-world evidence before funding decisions are made.

“The companies that invested in evidence generation… are now positioned to benefit disproportionately,” the report noted, while those that have not face increasing difficulty securing both funding and payer support.

The implications were likely to resonate beyond the investment community, particularly as governments and health systems grappled with how to integrate digital technologies into publicly funded care.

The report’s findings suggested digital health was increasingly being treated more like traditional medical products, subject to the same demands for clinical validation, cost-effectiveness and system integration.

Another notable trend was the decline in corporate partnerships, which fell 21% year-on-year globally.

Rather than signalling reduced engagement, the report argued this reflected a shift away from pilot programs toward deeper, more commercially substantive relationships.

“The era of signing 10 pilot agreements … is over,” it stated, with health systems and corporates now seeking embedded, contractually committed partnerships.

Geographically, the US continues to dominate the market, accounting for 76% of global venture capital, while the Asia-Pacific region has seen a significant cooling in investment activity.

For Australia and the broader region, this may raise questions about the sustainability of local digital health ecosystems in an environment where capital was increasingly concentrated in fewer markets and fewer companies.

Taken together, the data pointed to a sector undergoing rapid maturation. After a period defined by rapid growth and experimentation, digital health was entering a phase characterised by consolidation, discipline and a stronger focus on demonstrable value.

As the report concluded, the market is no longer rewarding ambition alone.

“Digital health … rewards proof,” it said.

Read the full report here.