The government has introduced legislation to outlaw a particular behaviour, but no legislation has been proposed to tackle the underlying design flaw that made it prevalent.

Australia’s four-tier private health insurance framework, Basic, Bronze, Silver and Gold, is producing a system-level outcome that is functionally inconsistent with the community rating principle enshrined in legislation.

The cause is a design problem.

Health fund modelling assumptions would have been based on consumers continuing to hold Gold tier products. However, ongoing cost-of-living pressures have forced healthcare consumers to compromise on cover, often without the health literacy needed to fully appreciate what they have traded off for what was perceived as affordable.

Now, the industry’s own peak body, Private Healthcare Australia, is publicly asking the government to fix it.

The numbers are stark.

Since 2019, the privately insured population choosing Gold hospital membership has shrunk from 55% to a historic low of just 31%, a 24% drop in six years.

Members Health, representing 25 not-for-profit funds, has described this as a potential ‘Gold death spiral’: ever-increasing costs making comprehensive cover unaffordable for all but the wealthiest or most unwell, effectively creating a two-tiered system within private health.

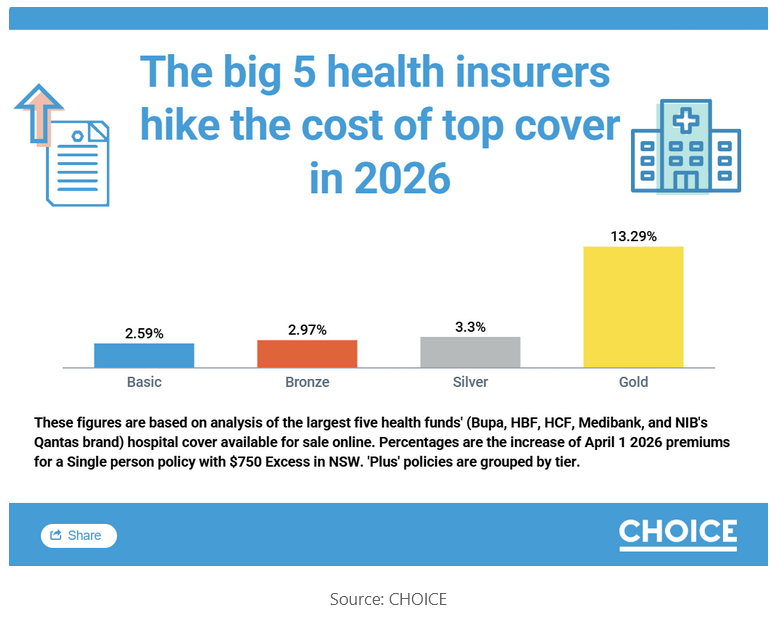

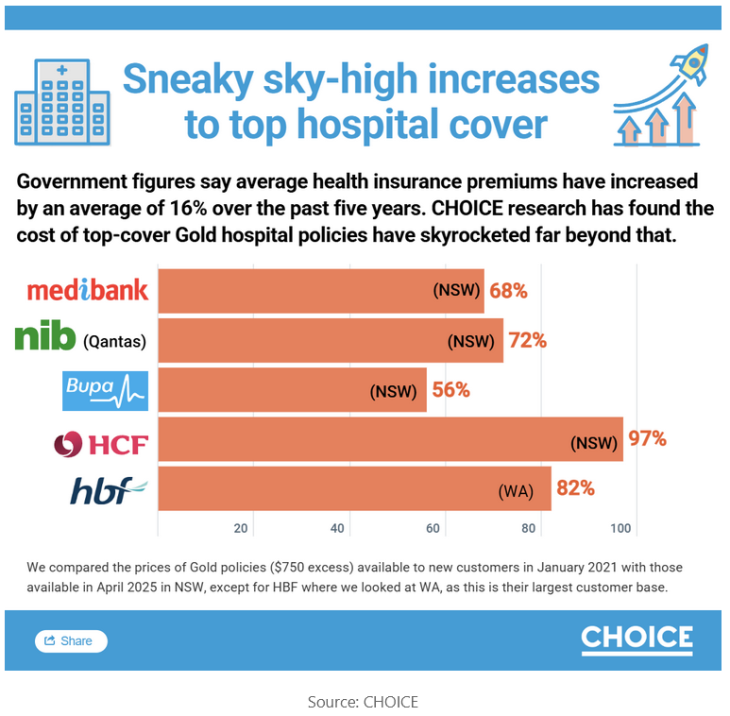

From 1 April 2026, a single person in NSW will pay an average of $439 per month for Gold tier hospital cover. Over five years, Gold premiums have risen 71%, far exceeding the government-approved average of just 16% across all tiers and all private health insurers over the same period.

Community rating is a statutory obligation, not an industry principle

Section 55-5 of the Private Health Insurance Act 2007 (Cth) prohibits insurers from discriminating between policyholders on the basis of “the suffering by a person from a chronic disease, illness or other medical condition” or “the frequency with which a person needs hospital treatment”.

The tier architecture produces a system-level outcome that is functionally equivalent to what the statute prohibits at the individual level.

While hospital psychiatric services, rehabilitation, and palliative care are mandatory inclusions across Bronze, Silver and Gold, restricted benefits apply for Bronze and Silver. For the Basic tier, they may not be covered at all.

In a public hospital, the restricted benefits are less of an issue. In a private hospital, a Bronze or Silver member requiring admission for psychiatric treatment, rehabilitation, or palliative care may face a significant out-of-pocket expense to cover the gap between the hospital charge and the restricted benefit payable by their health fund before any medical fees are considered.

In FY24, public hospitals delivered 79% of overnight mental health care nationally. It is likely that privately insured patients on Bronze and Silver tier policies were a material contributor to that load on a pressured public system.

In contrast, private hospitals delivered 77% of same-day mental health care nationally, as the out-of-pocket gap for same-day care is generally more manageable for Bronze and Silver members.

With one in five Australians aged 16 to 85 experiencing a mental health condition in any given year, a person with a known condition must hold Gold to access meaningful private hospital cover for that condition, while a person without one may think it is unnecessary.

A Bronze or Silver policyholder technically has hospital psychiatric services cover. In practice, they have cover that functions for treatment in the public system and is largely unusable in the private system without material financial exposure. The same applies to rehabilitation and palliative care.

The cover exists on paper. The benefit does not exist when needed.

The product tier decision by healthcare consumers is being driven by affordability constraints rather than anticipated health need (chronic disease, illness or other medical condition and treatment frequency), which is exactly the discrimination the legislation was designed to prevent.

It is occurring through the design of the subordinate legislation rather than through individual insurer conduct, but the effect on the healthcare consumer is the same.

Also in today’s edition:

- Seven Aussie hospitals make world’s top 250

- Balcony likely exposure point for RPA mould cluster, says report

- Telehealth tops DoHDA’s compliance priorities list

- Aged care resident charged with manslaughter

- Breast cancer patients face thousands in out-of-pocket costs, report finds

- ‘The next few years will bring uncertainty’: AHPRA

- Complaints about health insurance down 20%, says ombudsman

Phoenix rising – compounding the problem that legislation won’t fix

CHOICE has documented the practice of private health insurers closing an existing policy, and opening a new policy with the same or similar cover at higher prices which CHOICE has dubbed as phoenixing.

HCF’s February 2025 launch of Optimal Gold at a 34.6% markup, on the same day the federal minister for health announced the approved annual increase, earned HCF a CHOICE Shonky Award and prompted the government to introduce legislation to outlaw the practice, which is still before the House of Representatives but has not yet been passed.

From 1 April 2026, HCF’s Optimal Gold will increase by a further 25%, compounding from the higher base that phoenixing established.

Phoenixing is a response to structural claims pressure, not its cause. When the legislation passes, it will outlaw the behaviour but not tackle the structural reason that made it commercially rational and not unlawful in the first place, leaving the core problem intact.

PHA’s contradictory positioning

In a single March 2026 media release, PHA directed health fund members to lower tiers and called for a tier review to ensure it supports affordability by spreading the risk of high-cost care across a wider population.

Those two positions cannot both serve the same health fund member.

A member following PHA’s affordability guidance toward Bronze or Silver faces restricted benefits on hospital psychiatric services, rehabilitation, and palliative care in a private hospital, and potential exclusions on optional categories depending on the product chosen.

The reform call acknowledges that the system is producing the wrong outcome. The consumer advice directs members to the part of the system where that outcome is most acutely felt.

Related

The fix involves a tweak to the existing legislative framework

PHA has asked the right question.

Left unchanged, private hospital viability does not improve structurally, and community rating does not function as intended, which PHA promotes on its own website as a core principle of the system.

Amending the Private Health Insurance (Complying Product) Rules 2015 (Cth) to ensure that a Bronze or Silver policy must provide unrestricted cover for hospital psychiatric services, rehabilitation, and palliative care redistributes the risk pool in the way PHA is describing, restores the community rating principle for the three categories that need it most, and does so through an amendment to existing subordinate legislation. It does not require a wholesale redesign of the tier framework.

The government has introduced legislation to outlaw a particular behaviour, but no legislation has been proposed to tackle the underlying design flaw that made it prevalent.

The Consumer Sentiment Survey 2024 Final Report from the Consumers Health Forum found that one in 10 Australians could not afford the medical care they required. Most privately insured Australians hold Bronze or Silver cover.

The tier review PHA is now publicly requesting is the right vehicle. The mechanism is already in the rules. The question now is whether the tier review will address the design flaw, or only the symptoms it has produced.

Ed Butler is company director of PulseBridge Consulting, an independent private healthcare advisory practice supporting organisations to navigate complex operating environments, improve commercial performance, manage risk, and enable sustainable healthcare delivery.

This article was originally published on LinkedIn. Read the original article here.